Basic Income: A Sellout of the American Dream

Matt Krisiloff is in a small, glass-walled conference room off the lobby of Y Combinator’s office in San Francisco’s South of Market neighborhood, shouting distance from some of the country’s wealthiest startups, many of which Y Combinator has nurtured and helped fund. Krisiloff, who manages the operations of the tech incubator’s program for very early-stage companies, is explaining why it is committed to investing an amount said to be in the tens of millions of dollars in a venture that is guaranteed never to make a penny.

It’s the simplest business model conceivable: hand thousands of dollars over to individuals in return for nothing, no strings attached. Krisiloff insists he and his Y Combinator colleagues can’t wait to get started giving away the money. “This could be really transformative,” he says. “It may help change how humans, society, and technology all operate together in the future.”

The project is an experiment in what’s known as a “basic income”—or, when the money is given to entire populations, as a “universal basic income.” At its core, it’s a means for a government to alleviate poverty, replacing the myriad bureaucracy-bound safety-net policies in industrialized countries that struggle, with mixed results, to get money into the hands of those who most need it.

In the view of proponents, that money could also benefit people who aren’t poor but aren’t affluent either. They’d gain access to higher education, an escape route from oppressive jobs and relationships, greater opportunity to invest in their children’s well-being and education, and time to spend on artistic or other mostly nonpaying endeavors. “If people had that money, they’d be able to choose not to do the most notoriously low-paying jobs,” says Natalie Foster, a fellow at the Institute for the Future and New America California. “No one would have to be a workaholic only out of fear that they’d have nothing to fall back on if they stopped.” Wages, economic equality, and happiness would all climb, in this view.

Finland is studying a plan to give some 100,000 citizens nearly $1,000 a month as an experiment, and four cities in the Netherlands are about to start trial programs. The Canadian province of Ontario is preparing to run a trial, too, and a national test is under consideration. France’s parliament is discussing the topic, with some encouragement from the country’s finance minister. Meanwhile, Switzerland has come closest to instituting a national basic income. In June it held a referendum on giving its residents about $2,500 a month. It failed; only 23 percent of voters were in favor.

Is Silicon Valley just attempting to appease those left behind?

Progressives generally like such schemes, as long as they don’t leave the poor and jobless with less money than they get under existing safety-net programs. Many conservatives and libertarians are fans, too, thanks in part to the idea that a basic income would shrink government bureaucracy. (The Swiss proposal, however, drew opposition from many conservatives, in part because it was intended to be added on top of existing programs.)

In the United States, the basic-income concept is gaining renewed interest largely because a number of leaders in the technology industry are talking it up, especially in Silicon Valley and the San Francisco Bay Area. “There’s a lot of prominent chatter about basic income here right now,” says Roy Bahat, who heads Bloomberg Beta, a Bloomberg-backed venture capital firm in San Francisco. That chatter got louder after Y Combinator’s announcement this year that it will fund and run a basic-income experiment in a so-far-unnamed U.S. community. (The company has also said that a small pilot—not the main experiment—will take place in Oakland, California.)

For the Silicon Valley crowd, the prime motivation appears to be a concern that automation has been displacing jobs, and that increasingly sophisticated artificial-intelligence applications could accelerate the trend. One proponent is Jim Pugh, a data scientist and founder of ShareProgress, a technology company supporting nonprofits and social-impact organizations. “With self-driving cars on the streets here [in Silicon Valley] becoming a reality, there is growing concern about what an economy with widespread automation would look like,” he says.

What’s not to like about free money? Especially in the form of a poverty-relieving, quality-of-life-boosting grand scheme that gets a measure of broad-spectrum political support and commands enthusiastic attention from the most celebrated innovation community in the United States?

Well, there’s the fact that a universal basic income could add as much as $2 trillion in annual expenses to the U.S. budget. Then there’s the question of whether such a program might disconnect large swaths of our population from the positive aspects of working for a living—a potentially toxic side effect. And finally, there’s little convincing evidence that large-scale technological unemployment is actually happening or will happen in the immediate future. Advances are changing the types of tasks and skills in demand, displacing many workers from jobs that have become obsolete. But the massive, automation-fueled job displacement cited as the prime justification for a basic income won’t actually reach us for decades, assuming it does come. “The idea of a basic income is a good one in a world where robots do most of the work, but we probably won’t be there for 30 to 50 years,” says Erik Brynjolfsson, who researches the digital economy at MIT’s Sloan School of Management.

Proponents say a basic income is a way to liberate those who have struggled to find acceptable work: currently 7.4 million people are unemployed in the United States, another six million want full-time work but can only find part-time jobs, millions more have given up looking, and perhaps tens of millions have settled for jobs with low wages, skimpy benefits, or poor working conditions. But it can also be argued that the idea is a way of buying these people off, making it easier to avoid developing the education and training programs that would actually help alleviate income inequality and reverse wage stagnation. Could it just be a way to give up on providing the wide access to decent jobs that has long been considered an essential element of a healthy society? Or, to put it more bluntly: at a time when the tech economy is generating huge amounts of wealth, is Silicon Valley just attempting to appease those left behind?

Demogrant

Calls for a basic income date back at least to the early 16th century, when the philosopher Thomas More, objecting to England’s policy of executing thieves, suggested reducing poverty by giving a little money to all, regardless of employment. But the idea didn’t get much traction until the end of World War I, when the British mathematician and philosopher Bertrand Russell and the “social credit” movement won it some public support in both the U.K. and Canada. In the 1930s, the British Labour Party grabbed the baton, calling its basic-income plan a “social dividend.”

How much would a basic income cost? The simple answer is: a lot.

In the United States of that era, the New Deal focused on providing jobs through public works programs, so there was little interest in simply handing over money to the population. But the libertarian economist Milton Friedman revived interest in the early 1960s by calling for a “negative income tax” that would replace the much more complicated safety net of federal antipoverty programs and give the poor more control over their own finances. Martin Luther King Jr. was a supporter, too. In 1968 more than a thousand economists signed a petition for a basic-income scheme. President Richard Nixon obliged by trying to push through a “Family Assistance Plan” that was in most ways a basic income. Supported by a majority of the public and endorsed by most newspapers, Nixon’s plan sailed through the House of Representatives. It died, however, in the Senate, where conservatives balked at the cost and liberals wanted a higher payout and no work requirement. The 1972 Democratic presidential candidate, George McGovern, then got into the act, briefly including in his platform a $1,000 “demogrant” to all citizens. But the safety-net-shredding Reagan era killed all talk of a basic income in the U.S.

The current revival in this country can be traced to the fear of some in the tech community that digital technologies are destroying jobs. One important early booster was ShareProgress’s Pugh, who became interested in basic-income schemes three years ago after stumbling across an account of European experiments with the approach. He started writing articles and organizing events to promote support for it in Silicon Valley and “got an unexpectedly strong response,” he says. Other articles and posts from the tech community started popping up, and when Y Combinator announced its experiment, support in that population crossed a threshold.

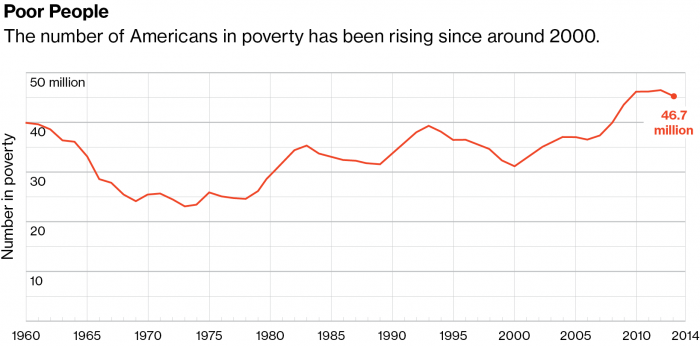

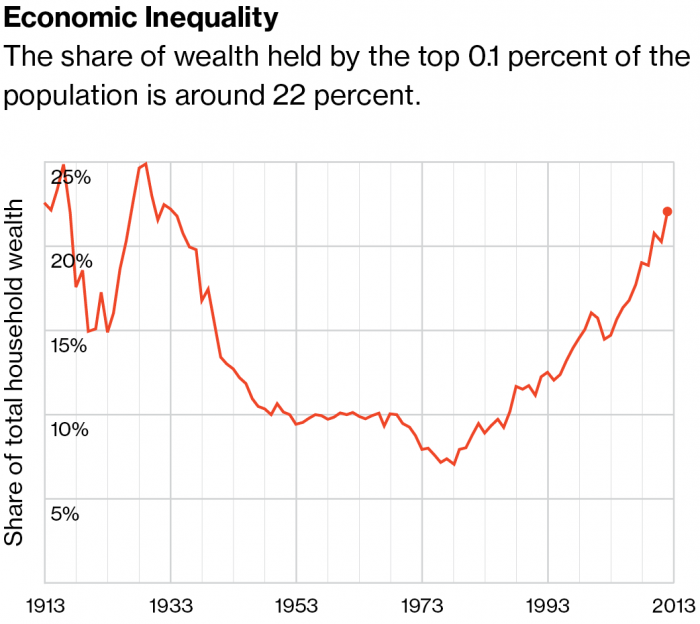

One reason the idea resonates is that many Americans are struggling economically. About one in seven people lives below the poverty line, according to the U.S. Census Bureau. For many more, other financial pressures loom. By all accounts, middle-class jobs that don’t require college degrees or advanced training are becoming harder to find, leaving many people who could once have held a good job in lower-paying work with less security. Meanwhile, the top 0.1 percent of Americans now account for more than 20 percent of the country’s wealth.

It’s hard to live in Silicon Valley without sensing the growing inequality. Chuck Darrah, a San Jose State University anthropologist who specializes in the ethnography of the tech industry, is a longtime Mountain View resident, and he has seen the value of his home quadruple to $2.3 million since 1998. In a walk around the town, he can point out other houses whose values are similarly staggering. Gentrification has forced the less affluent into exile, sending them far not only from their former homes and schools but also from the region’s stronger job markets. “Every bit of research shows Silicon Valley splitting apart faster than the rest of the country,” he says.

No wonder addressing poverty and job loss is on the minds of those in the technology crowd—when they aren’t hard at work coming up with apps that will help make it possible to automate some task or access some service that once required an employee. Combine the concern about AI-driven job displacement with the tech community’s drive to solve difficult problems through radically new approaches, and it’s not surprising that the idea of a basic income has become Silicon Valley’s latest obsession. Add to that a deep skepticism that government is capable of solving significant problems. And then throw in an awareness that the wealth tech workers are creating for themselves and the rest of the affluent minority is driving inequality to a point that could cause social unrest.

“Earlier in U.S. history we saw the rise of an enlightened capitalism that supported the growth of an empowered union movement, in part because some capitalists reasoned that it would reduce the chances of workers turning to socialism,” says David Grusky, who runs Stanford’s Center on Poverty and Inequality. “This is another moment in history in which there may be some diffuse anxieties about long-term unrest.”

Sticker shock

How much would it actually cost? The simple answer is: a lot. Economists are quick to point out that whatever savings might result from cutting out the existing safety-net bureaucracy, they are likely to be far outweighed by the cost of handing an annual check for, say, $10,000 to every adult in America. (Proposed amounts vary, of course, and are likely to be adjusted for those supporting children. It’s generally assumed that existing health-care financing programs would remain in place, as would Social Security.) A rough calculation suggests that a $10,000 basic income, enough to lift the vast majority of Americans above the poverty line, would be at least twice as expensive as current antipoverty benefits and overhead, adding between one and two trillion dollars to the federal budget. Halving the size of the check would go a long way toward solving that problem, but that would leave millions below the poverty line with fewer other programs to help.

Beyond the price, there are the worries about the social and cultural impact of taking so many people out of the workforce. Luther Jackson, a program manager at Nova, a nonprofit workforce development agency in Silicon Valley’s Sunnyvale, says he constantly sees evidence that job loss can mean much more than a missing paycheck, deeply depressing self-esteem and overall outlook. A weekly meeting of job seekers can become intensely emotional, he says: “It can be like a revival meeting. People are searching to understand who they are and how they fit in.” Indeed, the idea of addressing joblessness with money instead of jobs is an ironic one for the tech crowd to embrace, notes San Jose State’s Darrah. “They want this supposedly great solution for others, not themselves,” he says. “They thrive on work.”

But the concern that people will lose the incentive to work is overblown, say supporters of a basic income. Their claim goes this way: since the payout is likely to be far from generous, perhaps barely enough to live on, most people will probably choose to supplement their checks with work. The basic income will free them to pursue jobs with better pay, benefits, and conditions, or to look for more meaningful work—even if that work is lower-paying or nonpaying, such as staying home to take care of children or trying to develop an invention.

An ideal outcome, says Stanford’s Grusky, would be for low-skilled workers to invest the money from a basic-income program in training that equips them for higher-skill jobs—and for parents to invest it in early education for their children. “Right now those opportunities are more available to the rich,” says Grusky. “A basic income could allow the poor to buy those opportunities.”

And even if that didn’t happen and much of the population did take the money and drop out or get forced out of the workforce, the societal ties that today are rooted in work might be replaced by new ones, he says: “It could lead to a massive cultural revolution around the meaning of life.”

Risky bet

It may be true that new institutions and cultural attitudes are waiting in the wings to free us from our psycho-social attachment to work once a basic income frees us from our economic dependence on it. And it may be true that people who receive a basic income won’t stop working but will simply use the money as a springboard to more rewarding work. These seem like risky bets, though.

In fact, an annual survey by the Bureau of Labor Statistics shows that the main way the unemployed tend to use the time freed up by not working is in watching TV and sleeping, not inventing new products or mastering new skills. In theory, real-life experiments can help settle the question of what happens to people and communities when basic-income checks start coming in. And there have been several such experiments. In practice, however, the results have tended to provide fodder for both sides.

Large studies that took place during the Nixon administration in major U.S. cities including Denver and Seattle, as well as a big experiment in Manitoba, Canada, produced results supporting various researchers’ claims that people who receive a basic income work less or work more, and that families and communities were made more stable or less stable. Critics say the studies ended before the true benefits or costs could be realized, that the checks were too small to produce clear results, that the people involved weren’t a representative sample, or that the findings were misanalyzed. The experiments that will take place in other countries may not be any more conclusive: doubters are already dismissing them as less than relevant to conditions and attitudes in the United States. Even the Y Combinator experiment has been criticized as too limited in time and scope to offer a sense of the idea’s larger economic and social impact.

It’s not just that a basic income would be a risky bet based on murky data. The bigger objection is that it’s an unnecessary bet. Existing safety-net programs could be expanded and tuned to eliminate poverty about as effectively but much less expensively, and they could continue to focus on providing jobs and the incentives to take them.

The disadvantage of existing programs is that they generally phase benefits out as people make more money from jobs. That can have the perverse effect of discouraging work. The Earned Income Tax Credit, or EITC, is structured to solve that problem by ensuring that after-tax income always rises with pay, while still taking care that no benefits go to those who earn enough to live comfortably without them. For a married couple with three or more children, the maximum EITC is $6,242, reached for incomes from $13,870 to $23,630; if the credit exceeds the total tax bill, the balance is paid out as a tax refund. The credit is gradually phased out as income climbs above $23,630.

Robert Gordon, an economist at Northwestern University, believes the best course is to expand and improve existing safety-net programs, especially by increasing the EITC. “I’d make benefits more generous to reach a reasonable minimum, expand the Earned Income Tax Credit, and greatly expand preschool care for children who grow up in poverty,” he says. If all that happened, he adds, there’d be no need to consider the massive costs of a basic income. (Milton Friedman’s proposed negative income tax boiled down to a plan more or less equivalent to Gordon’s, phasing out as work income increased.)

We aren’t yet close to running out of jobs, so why go through so much expense to make it easy for people to opt out of the workforce? “We have an economy that right now is creating hundreds of thousands of jobs per month,” says Gordon. “It may be that many job seekers aren’t located where most of the jobs are, or lack the training to hold them.” But, he argues, those are problems that may be solvable without making tens of millions of people dependent on government paychecks.

If automation, software, and services based on artificial intelligence do eliminate huge numbers of jobs someday, the same developments will probably give a tremendous boost to wealth creation and prosperity. Funding a basic income with that wealth makes perfect sense—but doing it now doesn’t, says MIT’s Brynjolfsson. “While automation is replacing many jobs, it’s also creating new ones,” he says. “There’s still plenty of unmet needs and work to do, so the right strategy for the current situation is to prepare people for those new tasks.” And for now, says Brynjolfsson, “we’re not rich enough to afford a basic income that will provide everyone with a decent standard of living without having to work.”

David H. Freedman’s most recent book is Wrong: Why Experts Keep Failing Us.

Keep Reading

Most Popular

Large language models can do jaw-dropping things. But nobody knows exactly why.

And that's a problem. Figuring it out is one of the biggest scientific puzzles of our time and a crucial step towards controlling more powerful future models.

How scientists traced a mysterious covid case back to six toilets

When wastewater surveillance turns into a hunt for a single infected individual, the ethics get tricky.

The problem with plug-in hybrids? Their drivers.

Plug-in hybrids are often sold as a transition to EVs, but new data from Europe shows we’re still underestimating the emissions they produce.

Stay connected

Get the latest updates from

MIT Technology Review

Discover special offers, top stories, upcoming events, and more.